What Western Businesses Can Learn from Japan's Cashless Ecosystem

How Japan went from cash-obsessed to cashless leader—and what global businesses can apply today

Japan was late to the cashless party. While Sweden was eliminating cash and China’s mobile payment apps dominated daily life, Japan remained stubbornly attached to physical currency well into the 2010s. Cash represented over 75% of transactions as recently as 2018.

Fast forward to 2025: Japan’s cashless payment ratio hit 42.8%, with mobile payments Japan leading the charge through platforms like PayPay (70 million users) and integrated transit systems like Suica handling everything from train fares to coffee purchases. The transformation happened in under seven years—one of the fastest shifts in any developed economy.

For Western hospitality and retail executives watching digital transformation Japan unfold, the question isn’t just “what happened?” but “what can we replicate?” The answer reveals strategic lessons applicable far beyond Tokyo’s streets.

Lesson 1: Solve an Unavoidable Problem First, Expand Later

The Japan Model:

Suica didn’t launch as a payment platform—it solved train boarding congestion. In a country where punctuality is sacred and millions navigate Tokyo’s transit network daily, eliminating the friction of ticket purchases was non-negotiable. Once commuters habitually tapped their cards for trains, extending that behavior to convenience stores, vending machines, and restaurants became natural.

Today, over 100 million Suica cards have been issued, and the system is accepted at over half a million retail outlets nationwide. The transit card became a de facto payment infrastructure not through aggressive marketing, but through solving one critical daily friction point first.

The Western Opportunity:

Most Western payment innovations start with retail transactions—a “nice to have” improvement. But consumers already have credit cards that work fine. The friction isn’t painful enough to change behavior.

Instead, identify the unavoidable interaction in your customer’s journey. For hotels, it might be check-in/check-out. For restaurants, it could be splitting bills among groups. For retailers, perhaps returns and exchanges. Build a frictionless solution there first, then expand the payment functionality once the habit forms.

Suica started with trains, expanded to retail: Over 100 million cards now handle everything from subway fares to shopping

Example: A hotel chain could launch a mobile key system that also handles minibar purchases and spa bookings. Once guests habitually use the app for room access (unavoidable), adding restaurant reservations and checkout becomes a natural extension—not a separate payment app fighting for attention.

Lesson 2: Remove Merchant Friction at All Costs

The Japan Model:

PayPay’s explosive growth—reaching 70 million users and processing one in five cashless payments nationwide by 2024—wasn’t primarily about consumer features. It was about making merchant adoption trivially easy.

The barrier to entry? A printed QR code. No expensive terminals. No complex POS integration. No merchant fees during initial rollout. A street food vendor or rural farmers’ market stall could accept digital payments within hours, not weeks.

This contrasts sharply with traditional card networks requiring hardware investments, setup fees, and technical integration. Japan fintech trends show that the payment provider who makes merchant onboarding effortless wins the network effect race.

The Western Gap:

In the US and Europe, payment innovation often focuses on consumer convenience (Apple Pay, Google Pay) while merchants still need expensive terminals and navigate complex fee structures. Small businesses—restaurants, independent hotels, local retailers—often can’t justify the investment.

The result: fragmented acceptance. Your innovative payment solution might work at Marriott but not at the boutique hotel down the street, limiting utility and adoption.

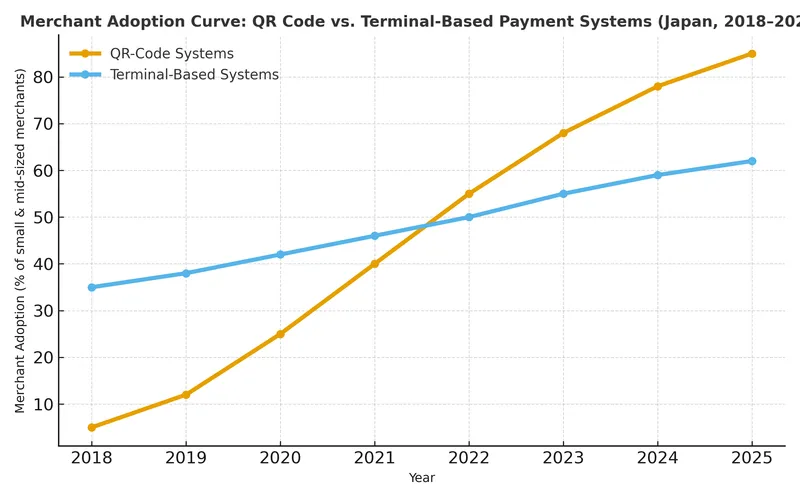

Figure: QR-code payment adoption surged from roughly 5% to 85% of small and mid-sized Japanese merchants between 2018 and 2025,

while terminal-based systems grew more slowly—from 35% to 62%.

The low hardware cost and ease of onboarding made QR codes the clear winner for rapid digital payment adoption.

The Strategic Shift:

Prioritize merchant simplicity over consumer features initially. Can a restaurant start accepting your payment solution with just a smartphone and a printed code? Can a small hotel integrate without IT support?

The unified QR standard “JPQR” introduced in 2019 exemplifies this approach—one code accepting multiple payment services, eliminating merchant confusion. Instead of cluttering counters with separate codes for each app, merchants display one, reducing resistance to adoption.

Example: A restaurant payment platform could provide tablets pre-configured for tableside payment, QR codes for customer self-pay, and automatic integration with existing POS systems—whichever the merchant prefers. The key is removing any excuse for “it’s too complicated.”

Lesson 3: Integrate Vertically, Not Just Horizontally

The Japan Model:

PayPay didn’t stay a payment app. By 2025, it evolved into a financial super-app offering banking through PayPay Bank, securities trading, insurance, and mini-apps for food delivery and utility payments. Users can pay a utility bill, split a restaurant check, buy train tickets, check bank balances, and invest in stocks—all without leaving the PayPay ecosystem.

Similarly, JR East’s “Suica Renaissance” plan transforms the transit card into a multifaceted digital lifestyle platform with QR payments, peer-to-peer transfers, online fare subscriptions, and personal finance tools integrated into one cloud-based system.

The digital transformation Japan strategy isn’t about doing one thing well—it’s about becoming the central platform for customers’ financial lives.

PayPay evolved from payments to super-app: Banking, securities, insurance, and utilities—all integrated in one platform

The Western Limitation:

Most Western payment solutions remain horizontal—they handle transactions but don’t integrate into broader customer lifecycles. Your hotel payment system processes checkout but doesn’t connect to loyalty programs, booking platforms, or post-stay services. Your restaurant payment app splits bills but doesn’t handle reservations, waitlist management, or catering orders.

This creates fragmentation. Customers juggle multiple apps: one for booking, one for payment, one for loyalty points, another for customer service. Each additional app reduces engagement.

The Integration Imperative:

Think ecosystem, not transaction. How can your payment solution become the hub for related services?

Hospitality example: A hotel payment platform could integrate:

-

Mobile check-in and room keys

-

On-property purchases (spa, dining, activities)

-

Loyalty point tracking and redemption

-

Local experience booking (tours, transportation)

-

Post-stay services (photos, dry cleaning delivery)

When payment becomes the connective tissue for the entire guest journey, you create stickiness. Guests won’t abandon the platform because it’s no longer just about paying—it’s about accessing everything.

Retail example: A retail payment app could expand into:

-

Inventory checking and product reservations

-

Personal shopper scheduling

-

Seamless returns and exchanges

-

Subscription management for regular purchases

-

Community features (style advice, product reviews)

Japan’s mobile payments ecosystem shows that the winners aren’t necessarily the best payment processors—they’re the platforms that make payments one feature of a comprehensive service.

Lesson 4: Make Cross-Border Seamless from Day One

The Japan Model:

Japan recognized early that payment isolation limits growth. By 2025, PayPay integrated Ant Group’s Alipay+ platform, allowing users of 26 overseas e-wallets from China, South Korea, Thailand, Malaysia, Singapore, Philippines, and more to scan PayPay’s QR code and pay in their local currency.

In September 2025, WeChat Pay users from China were enabled to pay at any PayPay-accepting store in Japan. One merchant QR code unlocks customers from across Asia—no separate terminal for Chinese tourists, Korean visitors, or Thai travelers.

The impact is tangible. Japan saw 3.4 million international arrivals in August 2025 alone, the highest single month ever. These tourists want to spend using familiar payment methods, not fumbling with currency exchange or foreign transaction fees.

JR East launched “Welcome Suica Mobile” in March 2025, allowing international visitors to set up a digital transit card and preload yen before arriving in Japan—eliminating airport confusion entirely.

The Western Blind Spot:

Most Western payment systems optimize for domestic transactions. A US hotel’s payment app works great for American guests but offers no advantage to international visitors, who default to credit cards with foreign transaction fees. European restaurant payment platforms don’t connect to Asian mobile wallets, missing the spending power of tourists from China, Japan, and Korea.

This matters increasingly as international travel rebounds. Your most valuable customers might be visitors who expect to pay with Alipay, PayPay, or KakaoPay—methods your system doesn’t recognize.

26 foreign e-wallets now accepted via PayPay integration—Chinese, Korean, Thai, Malaysian, and Philippine tourists pay in local currency at Japanese merchants.

The Global Strategy:

Build payment solutions with cross-border interoperability from the start, not as an afterthought. Partner with international payment networks. Support currency conversion transparently. Enable tourists to use their home country wallets at your properties.

Hospitality example: A hotel chain could integrate with Alipay+, WeChat Pay, and regional Asian wallets, allowing Chinese guests to pay with familiar methods while seeing charges in yuan. This isn’t just convenience—it increases spending. Tourists spend more when they can track expenses in their native currency and use trusted payment methods.

The Japan fintech trends demonstrate that payment interoperability isn’t a technical challenge—it’s a strategic decision. The infrastructure exists through platforms like Alipay+ and emerging JPQR-QRIS linkages between Japan and Southeast Asia. The question is whether Western businesses will adopt these networks or remain isolated.

Lesson 5: Government Partnership Accelerates Transformation

The Japan Model:

Japan’s cashless surge wasn’t purely market-driven. The government set a 40% cashless ratio target by 2025, then deployed policy levers to achieve it:

-

Cashback incentives: A 2019 program offered 2-5% rebates on digital payments at small merchants, driving adoption

-

My Number Points: Citizens linking their national ID to payment services received bonus points, bringing millions of older residents into the ecosystem

-

Unified standards: The JPQR system reduced merchant confusion by allowing one QR code to accept multiple services

-

Digital salary legalization: April 2023 rules allowed wages to be deposited into digital wallets, not just bank accounts

The result: Japan exceeded its 40% target ahead of schedule, reaching 42.8% in 2024.

The Western Approach:

Western markets largely leave digital transformation to private competition, with minimal coordinated policy support. The result is slower, more fragmented adoption.

The Strategic Opportunity:

Engage with policymakers and industry associations to advocate for standards and incentives that benefit the entire ecosystem, not just individual companies. Japan’s JPQR standard, for example, made all participating payment providers stronger by simplifying merchant adoption.

For hospitality and retail, this might mean:

-

Lobbying for tax incentives for businesses adopting integrated payment systems

-

Supporting industry-wide standards for payment interoperability

-

Partnering with tourism boards to create seamless visitor payment infrastructure

-

Advocating for regulatory clarity on digital wallets and cross-border transactions

When policy and innovation align, transformation accelerates. Japan proved that collaborative infrastructure beats fragmented competition.

From 25% to 42.8% in seven years: Government targets and incentives accelerated Japan’s cashless transformation

The Implementation Roadmap

These lessons aren’t theoretical—they’re actionable. Here’s how to apply them:

For Hospitality:

-

Start with unavoidable guest touchpoints (check-in, room access)

-

Make adoption zero-friction for properties (no complex IT requirements)

-

Integrate payment with booking, loyalty, and experiences

-

Partner with international wallet networks before peak travel season

-

Work with tourism authorities on visitor payment initiatives

For Retail:

-

Identify the most painful customer friction (returns? Checkout lines?)

-

Deploy merchant-friendly solutions (QR codes, simple terminals)

-

Build vertical integration (payment + loyalty + inventory + services)

-

Enable cross-border commerce for international customers

-

Advocate for industry standards that benefit all participants

Your Next Step

Japan’s cashless ecosystem transformation happened in under a decade—from laggard to leader. The strategic lessons are clear: solve unavoidable problems, remove merchant friction, integrate vertically, enable cross-border seamlessness, and align with policy support.

But execution requires detailed market intelligence. How do Japanese platforms technically integrate banking and payments? What were the actual merchant acquisition costs for PayPay’s QR rollout? Which cross-border partnerships deliver the highest ROI?

Download our complete whitepaper: Japanese Consumer Payment Technologies: Innovations and Trends (2024–2025) for comprehensive analysis including:

-

Detailed competitive landscape and market consolidation dynamics

-

Cross-border payment integration and international wallet partnerships

-

Regulatory framework, standards development (JPQR), and policy incentives

-

Consumer adoption patterns and demographic trends

-

Platform integration strategies across transit, retail, and financial services

-

Growth opportunities in tourism and financial inclusion

The next wave of digital transformation won’t be isolated payment improvements—it will be integrated ecosystems that connect every customer touchpoint. Japan is writing the playbook. The question is whether your business will apply these lessons before your competitors do.

Want the full story on Japan’s cashless revolution?

Download Japanese Consumer Payment Technologies: Innovations and Trends (2024–2025) and uncover the data, strategy, and lessons behind Japan’s transformation into a cashless leader.

Download the Whitepaper